MathFinance Newsletter Editorial

Mixed Local Volatility Model Boosts Distribution of Exotics

As a market maker for FX Derivatives, and especially flow products on a single dealer platform, one needs the best trade-off between precision and speed in one’s exotics model. A Mixed Local Volatility (MLV) model is a simplified, yet powerful version of the full-fledged Stochastic Local Volatility (SLV) model. It ignores correlation between spot and volatility (which is common in FX); the skew is generated exclusively from local volatility, and the stochastic volatility process is simplified into a discrete set of volatility states. The key features include:

- MLV is more than 10 times faster for calibration and pricing than SLV.

- It allows flexible calibration to term-structure of Double-No-Touch (DNT) contracts.

- It is arguably the market standard for pricing a large range of 1st generation exotics.

How is volatility modeled in SLV and MLV?

Ignoring drift (interest rates and forward rates), the general concept of an SLV model is using a product of a local and a stochastic volatility model, stochastic for the model dynamics and to reflect non-deterministic volatility, local to fit the model to a given vanilla options volatility surface.

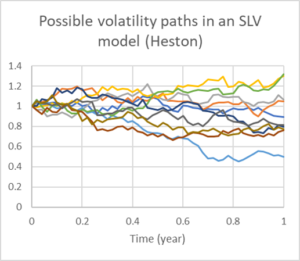

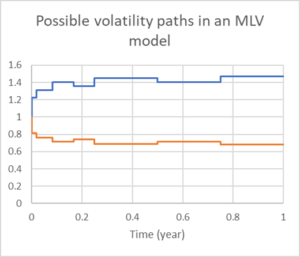

The choices for the stochastic volatility is typically a diffusion process in SLV models, indicated by infinitely many paths on the left hand side in Figure 2. For MLV, one can think of tossing a coin and generate a low volatility state or a high volatility state.

|

Volatility driven by a diffusive process (e.g. Heston) with continuous distribution

|

Volatility is stochastic, but randomness only in t=0 and with a discrete distribution |

Figure 1: Volatility Processes in SLV and MLV

How do traders mark an MLV model?

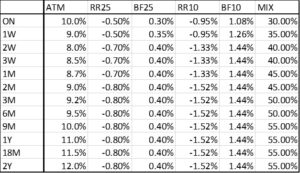

As a trader one either faces or distributes FX volatility market data in the form of At-the-money (ATM) volatilities, Risk Reversals (RR) and Butterflies (BF) for 25-delta and 10-delta strikes for the usual tenors as listed in Figure 3.

Figure 2: Volatility Market Data and MLV Mixing Factors (MIX)

A trader’s job is then to mark the term structure of mixing factors empirically, for example, the 1M mixing factor of 45% means that

45% of BF25 is generated by stochastic volatility (or mixture)

55% of BF25 is generated by the local volatility

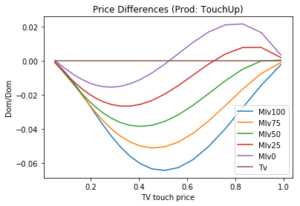

Traders mark MIX to match a set of One-Touch (OT) or Double-No-touch (DNT) contracts. Figure 3 shows the difference of MLV-based OT prices and their corresponding theoretical value (TV) as a function of the TV, an illustration generally referred to as the OT-moustache. Different mixing factors (MIX) of 0%, 25%, 50%, 75% and 100% generate different price differences. The trader chooses the MIX that would be represent the market prices of OT contracts. Notice that the interbank bid-offer spread is about 2% in USDJPY, which is one unit block on the y-axis, thus the choice of MIX is crucially important when running an automatic trading platform.

Figure 3: One-Touch Moustache in the Mixed Local Volatility Model with various mixing factors

It prices of first generation exotics are not readily available, a statistical estimate of MIX can also be obtained by looking at historical correlation between spot and RR25.

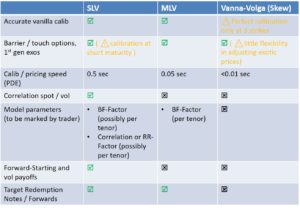

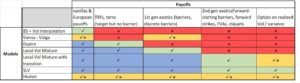

Comparison SLV / MLV / Vanna-Volga

I summarize the key features of the three most common industry exotics models in Figure 4. The vanna-volga approach, which was popular until the first decade, works mostly for first generation exotics, that here with many traps and inconsistencies. The only real advantage is really its calculation speed.

Figure 4: Features of SLV, MLV and Vanna-Volga Models

A trader can’t mark a vanna-volga model, but can mark an SLV or an MLV model. The MLV is easier to mark as there is only one mixing factor. MLV outperforms SLV in calibration and pricing speed, but would perform poorly for forward starting contracts and volatility derivatives like variance swap, volatility swaps, FVAs, or volatility options.

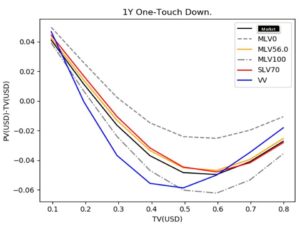

Example 1: USDJPY One-Touch (OT) under MLV and SLV

I reconsider the OT-moustache in Figure 5, with TV of a 1Y One-Touch with lower barrier on the x-axis and differences to TV on the y-axis.

Figure 5: Marking SLV and MLV to Market Prices of One-Touch Contracts

The dashed line originates from a fully local volatility model (MLV0) and indicates overpricing of the OT. The dash-dot line is a fully stochastic volatility model (MLV100) and indicates underpricing of the OT. The black curve represents market prices. A suitable fit of an SLV model in red can be obtained by an SLV mixing factor of 70% (SLV70). An equally suitable fit of the MLV model can be obtained by a mixing factor of 56% (MLV56). Note that the mixing factors generally differ depending on the model choice. Vanna-Volga (VV) in blue has a similar pattern, but still leads to mispricing of the OT contracts as it is often outside the market bid-offer.

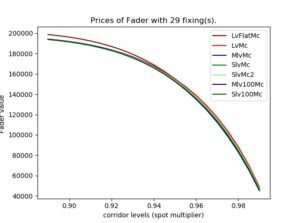

Example 2: Fader Call

Next I consider a fader call option with a notional proportional to the number of times the FX rate fixes in a pre-defined corridor, whose lower end is set by the spot multiplier and upper end is calculated symmetrically, e.g. 1.1 for a spot multiplier of 0.9. The prices generated by various SLV and MLV models are exhibited in Figure 6.

Figure 6: Fader Call Option Prices in Different Models as Function of the Corridor Size

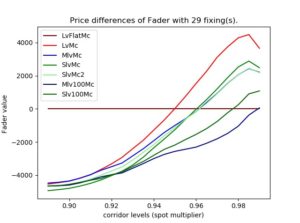

Since the prices overlap each other, it is better to consider the differences of the prices to TV in Figure 7. We observe that for wide corridors, all the models under consideration yield similar results, but for small corridors the differences are much larger. I conclude that model risk is not only a function of the product, but also of the contractual parameters of the product. Faders with small fade-in corridors will be priced differently in different SLV and MLV models. The way to go forward is to make the fader price at least consistent with first generation exotics by calibrating an MLV model with the appropriate MIX.

Figure 7: Fader Call Option Price Differences in Different Models as Function of the Corridor Size

And of course, the risk managers and model governance officers should be aware the model risk.

A parsimonious choice of model

An overview of which model I consider suitable for which product class is presented in Figure 8. Red colors refer to a too simple model and mispricing, blue indicates a too complex model and overkill, and green the right level of complexity. Yellow indicates borderline cases, e.g. a vanna-volga approach does not even work precisely for vanilla options, because the volatility is only correct for three strikes, but usually wing volatilities are too low. A pure Heston model, while studied intensely in the academic literature does not really perform satisfactory for any product.

Figure 8: Model/Product Matrix

In summary: MLV is a simplified version of SLV

- The stochastic volatility process is discretized into a small number of volatility states.

- Zero correlation between spot and volatility is assumed (common assumption in FX).

- MLV contains the necessary flexibility to calibrate to a large range of 1st generation exotics and most of the target forwards family.

- Calibration and pricing is very fast, suitable for structuring and a flow trading environment.

MathFinance has experience with SLV and MLV models; for further information and case studies please get in touch with us.

Uwe Wystup

MathFinance AG

References

There are not many papers out there on Mixed Local Volatility Models, but some worth reading include

- Bruno Dupire. Pricing with a smile. Risk, 7(7), 18-20.

- Yong Ren, Dilip Madan, Michael Qian Qian: Calibrating and pricing with embedded local volatility models, Risk Magazine, September 2007, 138-143.

- Iain J. Clark: Foreign Exchange Option Pricing – A Practitioner’s Guide, Wiley Finance.

———————————————————————————————————–

MathFinance Conference 2020

1 October 2020

Online Webinar

MathFinance is excited to host its first digital conference. This year we have an excellent line-up of speakers from both the professional and academic world presenting relevant and cutting-edge topics in the world of quantitative finance. The focus of this conference is on topics in the realm of quantitative finance as well as artificial intelligence applications in quantitative finance.

For the first time we will have speakers and attendees that spans across three continents (North America, Europe and Asia) due to the combination of our flagship conference in Germany with that in Asia. This year we are excited to have the following distinguished speakers at our conference:

Dr. Bruno Dupire: Head of Quantitative Finance, Bloomberg

Dr. Jesper Andreasen: Head Quantitative Research, Saxo Bank

Dr. Jan Vecer: Charles University

Dr. Rolf Poulsen: University of Copenhagen

Dr. Adil Reghai: Head of Quantitative Research, Equity and Commodity Markets, Natixis

Dr. Jos Gheerardyn: CEO, Yields.io

Dr. Kay Pilz: CEO, Kinetic Mind

Dr. Natalie Packham: Berlin School of Economics and Law

Dr. Antonis Papapantoleon: National Technical University of Athens

Dr.Thorsten Schmidt: Senior Financial Engineer, MathFinance

Dr.Martin Keller-Ressel: Technical University Dresden

Dr.Patrick Kuppinger: Head Quant Group, Bank Vontobel AG

Dr.Nils Detering: University of California, Santa Barbara

For the agenda and registration process please visit:

https://mtf-old.ansichtssache.de/events/mathfinance-conference-2020/

————————————————————————————————————————————-

MathFinance Trainings

MathFinance is excited to offer in-house as well as external training courses on the following subjects:

– FX Options & Structured Products

– Machine Learning & Artificial Intelligence Applications for Financial Markets

– Equity Derivatives: Pricing, Hedging, Structuring & Risk Management

– Interest Rate Derivatives: Pricing, Hedging, Structuring and Risk Management

– Credit Risk Modelling: IFRS 9 & Stress Testing

For further details on our other offerings please visit:

https://mtf-old.ansichtssache.de/trainings/

Quant Job Positions

Deka Bank is looking for a Quantitative Analyst with focus on equity derivatives pricing and risk management. In addition to in-depth knowledge in this field the candidate needs strong C++ skills to reinforce the team implementing the pricing library.

If you are interested, you can find more details at:

https://www.deka.de/deka-gruppe/karriere/jobboerse/2020-1/mitarbeiter-wmd-quantitative-analysen

————————————————————————————————————————————-

Call for Papers

Special Issue on Artificial Intelligence, Machine Learning and Platform Innovation in Quantitative Finance (MathFinance Conference 2020)

Overview

Traditionally, Quantitative Finance has revolved around the development of parsimonious models that yield some economic understanding of financial markets. In recent years, there has been a change in this paradigm by embracing data-driven methods from AI and ML. Here are some reasons that explain this shift: greater amounts of financial data are available that require fast processing; financial analysis and computations are supplemented by non-financial data, such as textual data, in order to create new insights; data-driven methods allow to detect trends and market changes that would not be observed with a rigid model. At the same time, platform technology has taken over trading of spot and derivatives in financial markets. Pricing models, Greeks and risk calculation have to be faster and more accurate than ever before. The special issue welcomes contributions that explore innovative uses of AI / ML methods and platform technology in Quantitative Finance. These can involve economic, quantitative, computational and technological aspects.

Speakers and participants of the MathFinance Conference 2020 are encouraged to submit their work, but the special issue also welcomes contributions from the community.

Editors of the Special Issue

Prof. Dr. Natalie Packham, Berlin School of Economics and Law

Prof. Dr. Uwe Wystup, Managing Director, MathFinance

Instructions for Submission

For submission, authors are requested to access the access the Editorial Manager at the following URL: http://www.editorialmanager.com/dfin/default.aspx. Please answer ”Yes” when asked if your manuscript belongs to a special issue and select the special issue in the list that will pop up.

Potential authors are reminded that all papers that are finally accepted for this special issue will be subject to format restrictions complying with the publisher’s standards. To speed up publication, and to ensure a unified layout throughout the special issue, authors are kindly advised to use LaTeX. Springer’s LaTeX template (click here) can be used to prepare source files (please choose the formatting option “smallextended”). The authors are highly recommended not to modify the class file by introducing personal settings and/or definitions.

Important Dates

- Deadline for paper submission: 15 October

- First-round decisions: 15 November

- Deadline for second-round submission: 15 December

- Final decisions: January 2021

About Digital Finance

The journal is a top tier peer-reviewed academic and practitioner journal that publishes high-quality articles with a focus on digital finance and innovation as well as on the analysis of digital and internet innovations on financial services and the economy. The journal publishes theoretical or empirical, qualitative or quantitative papers of interest to academics, practitioners, and regulators with the emphasis on empirical, financial market, and investment innovation, financial policy research and recommendations related to improving the welfare in the digital economy. Further details on this journal are available on the Springer website: https://www.springer.com/42521